School Fee Planning Guide

It’s no secret that school fees are dauntingly expensive… and a long-term commitment for families.

While many parents adopt a ‘pay as you go’ strategy, putting a structured plan in place can help significantly.

This article will offer some guidance on what you could do to help ease the burden of private school fees. This article will be relevant for parents looking to fund primary school, senior school, boarding school, or university.

If you would prefer to directly consult an expert, feel free to contact us.

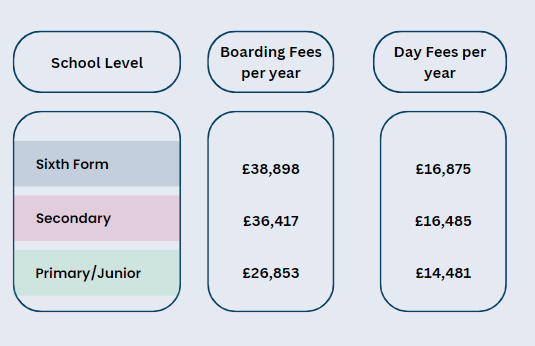

These fees are just the beginning. On top of regular fees, parents need to consider costs associated with school uniforms and trips, as well as extra-curricular activities such as music lessons, sports, drama… and not forgetting the tuck shop! These fees can add up to thousands per year.

This level of expense can put many people, even high earners, under considerable financial pressure. So, while many parents may wish to send their children to private school, the astronomical cost of education means that even those on higher salaries may struggle to afford it. Parents need to start planning how they will cover the costs as soon as possible.

The financial planning process cannot start early enough; perhaps even before children are born, you should start creating a fee plan.

Before making any investment decisions, it can also be worth speaking to the school to discuss options for funding in advance. Some private schools in the UK offer the option to pay in advance as a lump sum, and this can result in a discount on standard fees as well as protection from future fee inflation.

This is certainly something to consider, although typically the discount rate, if any, is not that attractive, and if managed correctly, the money could be invested to greater effect elsewhere..

We recommend suitable investment strategies for clients looking to save and invest for school fees. As and when money is needed for school fees, regular amounts can be withdrawn.

At Featherstone, we use cashflow modelling to assist with planning for the payment of school fees.

By investing tax-efficiently, funding private education for your children can become less of a burden.

Below, we will look at three straightforward strategies that could be suitable for parents saving for school fees while minimising tax.

Tax-Efficient Investment for School Fees

Investment ISA

A simple way to save for school fees in a tax-efficient manner is by investing within an ISA (Individual Savings Account). In this type of account, all capital gains and income are tax-free, meaning that money can grow free from tax, which can lead to a higher potential return.

By saving as much as possible into an ISA and investing across a diversified range of assets, parents could potentially build up quite a sum in the space of five to ten years, which could certainly help ease the school fee burden.

Aside from its tax-efficient nature, the other main advantage of an investment ISA is that it is an extremely flexible investment vehicle. Not only can investors hold a variety of different assets, including cash, funds, and individual shares, but money can be withdrawn at any time. This makes ISAs an ideal tax-efficient savings vehicle for a school fee savings plan.

Pension

Another option to consider, particularly for older parents, is investing in school fees within a pension scheme such as a Self-Invested Personal Pension (SIPP). Like an investment ISA, SIPPs offer a range of investment options and tax advantages.

Generally speaking, 25% of pension savings can be withdrawn tax-free at the minimum pension age, even if you are still working. The minimum pension age is 55, rising to 57 in April 2028. This means that if a parent had built up a SIPP worth £500,000, for example, at age 55, they could potentially withdraw up to £125,000 tax-free and put this money towards school fees.

Another benefit of saving into a SIPP is that tax relief is provided on contributions. Subject to certain allowances, personal pension contributions benefit from tax relief, in some cases up to 60%. For example, an individual earning £125,000 could make a gross pension contribution of £25,000 at a net cost of just £10,000.

Junior ISA (JISA)

A third option to consider is a Junior Investment ISA. This approach is a little different from the first two options because any money placed within a Junior ISA belongs to the child and cannot be accessed until the child turns 18. A risk of this strategy is that at 18, the child (now an adult) could decide to withdraw the funds for their own benefit… We have yet to witness an adult child pay for their own school fees! However, funds saved within a Junior ISA could potentially be used to support the cost of a gap year or university fees after age 18. Currently, the annual allowance for junior ISAs is £9,000 (2023–24).

Tax-Efficient Strategies Involving Grandparents

Even with the help of the tax-efficient saving and investment strategies mentioned above, many parents will still struggle to save enough money for private or independent school fees, given the substantial cost of private education. As a result, grandparents may offer financial help.

While there can be inheritance tax implications for grandparents paying fees directly to the school, there are several other ways for them to provide school fee support in a tax-efficient manner.

Below, we look at four popular tax-efficient school fee savings strategies involving grandparents.

Lump Sum Gifts

Lump sum gifts are a straightforward, tax-efficient option for grandparents to consider.

Gifts made by grandparents to their own children to pay for school fees may be subject to inheritance tax (IHT). However, provided the gifts fall within the annual exemption of £3,000 per grandparent per tax year, they will have no inheritance tax consequences other than diminishing the taxable value of the grandparents’ estate. If unused in the previous tax year, the £3,000 annual exemption can be carried forward, meaning that two grandparents could immediately gift up to £12,000 IHT free.

Larger sums can also be gifted free from IHT, as long as the grandparent survives for seven years after the gift is made, under the Potentially Exempt Transfer (PET) rules. If the grandparent did not survive the full seven years after making the gift, the amount gifted would use up some of their £325,000 IHT nil rate band.

Gifts out of Excess Income

Grandparents could also consider taking advantage of the inheritance tax exemption available for those with an income surplus to meet their needs. This is one of the more generous and often unknown IHT exemptions, and in many circumstances, it can be more effective than making a single outright gift.

To make use of this exemption, grandparents make a series of regular gifts to their children or grandchildren from their excess after-tax retirement income. If the conditions for the exemption are met, the gifts will be exempt from IHT immediately.

Setting up a Trust

Grandparents can help with the payment of school fees using trusts. Although parents can make gifts directly to their minor children, they are liable for tax on income of over £100 per year on the amount gifted. This restriction is in place so that parents cannot take advantage of their children’s tax allowances for their own gain. This rule, however, does not apply to gifts made by grandparents to their grandchildren, and the use of trusts allows for larger gifts to be made while retaining control over the decision-making process.

There are many different types of trust, but setting up a “Bare Trust” for a grandchild for the payment of school fees is straightforward. Bare Trusts are absolute trusts also known as simple trusts or, as the name implies, ‘naked’ trusts. Tax treatment is favourable, with assets treated as the property of the child and taxed within their own allowances accordingly. Given that children currently have an income tax allowance of £12,570 and a capital gains tax allowance of £6,000 (in 2023–24, reducing to £3,000 in 2024–25), there may be no tax to pay on capital or income within the trust. Any assets remaining in the trust pass to the child on their 18th birthday—perhaps to assist with further education costs or to fund a gap year. Gifts into Bare Trusts are treated as PETs, with no IHT to pay on the gift after a seven-year period.

Setting up a Family Investment Company

Family investment companies could be set up by grandparents with their grandchildren as shareholders.

Income generated from business assets, such as an investment or property portfolio, might be distributed in the form of dividends, which may be at a lower tax rate.

The incorporation and maintenance of family investment companies requires specialist advice and may be an effective structure for passing on intergenerational wealth tax efficiently.

School Fee VAT

The current VAT rules exempt the provision of education by ‘eligible bodies,’ which includes any registered independent schools and charities that provide education, from VAT. This means that independent school fees and services related to the supply of education, such as school meals, trips, boarding accommodation, after-school care, catering, and transportation, are currently all exempt from VAT.

However, the Labour Party has strongly proposed the idea of levying a 20% VAT on services related to independent school fees. This proposal would potentially impose a 20% VAT on the fees themselves, along with services like school meals, trips, boarding accommodation, after-school care, catering, and transportation provided by independent schools, while the provision of education itself would remain exempt from VAT. They would also see the end-of-business rate relief enjoyed by independent schools.

This will make school fees even more expensive…

Looking for help on your school fee planning?

The cost of private school can be daunting, but with proactive planning, you can make it more manageable. Our financial advisors have extensive experience creating customised school fee plans to fit families’ budgets and savings goals. We take the time to understand your unique situation and priorities when designing an optimal strategy. Whether you want to start saving now for future school years or need help covering current fees, we’re here to guide you. Book a call today

What are the benefits of school fee planning?

- It helps reduce the financial burden when fees are due

- Ensures funds are available for child’s education

- Avoids taking on education loans or debt

- It helps provide you with peace of mind

- Develops financial discipline through regular saving

- Allows invested funds to compound over many years

- Can provide tax advantages

- Secures child’s educational future without compromising other goals

Regulatory Information

This communication does not constitute tax or financial advice. All information is accurate at the time of writing. The value of investments can go down as well as up. Capital is at risk. Featherstone is a trading name of Featherstone Partners Limited, Old Brewhouse, Yattendon, Berkshire, RG18 0UE, which is authorised and regulated by the Financial Conduct Authority (799741) and registered in England (Company Number 11039522).

References

Independent Schools Council (ISC) Census (2022)

https://www.schoolguide.co.uk/blog/how-much-does-private-school-cost

https://www.isc.co.uk/research/annual-census/

Our Approach

At Featherstone Partners, we provide our clients with access to high-quality, niche investment funds that few private clients typically would have access to without us.

We believe that a portfolio consisting of various specialist fund managers based around the world, and focused on specific themes, is likely to outperform the generalist approach to wealth management that is often observed within the investment management industry.

Our clients enjoy the qualities of a smaller, friendlier firm, while benefiting from our team’s experience working at firms such as Goldman Sachs, UBS, GAM, Ruffer, and Close Brothers. Aligning our interests with those of our clients, we invest alongside them, and our founders, staff, families, and friends are among our largest (and smallest) investors.